It’s been a year and a half since I’ve done a full and formal spending and budget review. And I really need to get my ducks in a row because we’re expecting our first child in spring 2026! And with that, many more expenses, both foreseen and surprises I’m sure.

I pretty much need to completely overhaul my budget from the mid-year 2024 review; it’s almost comical how off target I’ve been. Some of that has been strategically accelerated spending to get out of the way before we have a daycare bill and other associated expenses for keeping a tiny human alive. I recently took two weeks off work to renovate our kitchen, and that’s hopefully the last big housing expense coming our way for a while. Our fixer-upper is nearly fixed up, and most remaining tasks will demand more in labor than materials.

So, let’s take a look at the numbers, sorted highest to lowest by actual spending in each category:

I’m not surprised to see my housing expenses so high, after all we did renovate an entire kitchen, and I was able to offset a respectable percentage of our new cabinets by selling the old cabinets and countertops. That said, I had a lot of moderate purchases add up over the last six months, some of which I forgot about until summarizing it all here.

Unexpected vet bills. An unexpected phone upgrade (my Google Pixel 7a battery swelled up and it was out of warranty with a battery replacement costing more than the phone value, so I bought an iPhone Pro outright and hoping to use it for at least 5 years). I bought some home workout equipment. I also bought some homebrewing equipment since my brewing activities have been relocated out of the new kitchen. Probably one major purchase every month really bloated my budget; nominally this is the most I’ve ever spent during a six month average, just beating out my year-end 2023 spending. Inflation-adjusted, it’s the second lowest, essentially tied with my six month spending average from December 2025:

One thing is clear, with an average of only $579.42 in monthly free cash flow, I need to pare my expenses back. Otherwise I will have to reduce my 401k contributions to fit in a daycare bill next fall, and I’d really rather not reduce my 401k. I value the tax-advantaged space it offers, and maxing it out has been the primary engine for most of my FIRE portfolio growth over the past decade. A few of my recent expenditures I believe were driven by the thought of buying something I’ve been thinking of getting now, before baby comes along and money gets tighter. I will definitely need to strongly evaluate any luxury consumerist purchases going forward, since I really don’t want to “bust my budget” in 2026 and end up with a negative free cash flow.

Budget Update, Net Changes, and Future Goals

I tried to take this information and distill it into an updated but more realistic budget; baby will bring more expenses (likely some of which I am overlooking) but I’m hoping we can avoid going crazy on baby gear through hand-me-downs and baby shower gifts. My dreams of going back to a lean, post-college budget are definitely over, however. Here’s the changes I made and the budget I’m hoping to stick to for the first half of 2026:

Here’s the rationale for all of the changes I made, in sequential order:

- While my mortgage payment is the same, utilities in Massachusetts are up since I last revised my budget, especially natural gas for heating.

- I never formally updated my budget to include my new car payment after my old one was totaled.

- I’ve guesstimated a baseline initial child cost of $500/month, so we will see how this shakes out and I know it will be increasing in fall 2026 when we start daycare.

- Groceries definitely seem to be increasing faster than the stated inflation rate of 2%; meat is up nearly 5% over the past 12 months according to BLS.

- Our cat is requiring more vet care and more prescriptions as he gets up there in age.

- I’ve been consistently over-budget in “Consumer Goods” for a long time, which is probably due to the fact that I use this as a catchall category for buying “stuff” (especially from Amazon) that doesn’t neatly fit into any other category. I’m increasing the budget amount, but I’ll try to stay mindful of every purchase.

- I broke out “Homebrewing” into its own category since it’s a consistent and recurring hobby expense. This may reduce “Alcohol/Bars” but probably not. I’m actually barely drinking alcohol, I’m both buying and brewing mainly non-alcoholic beer which I suppose while better for health, is worse for the wallet because it’s more expensive than regular beer, and one can drink more of it with no ill effects.

- My phone spending has been updated to the cost of my new prepaid T-Mobile plan. This new iPhone had better last me a long time.

- My student loans are paid off! This expense is eliminated and will be deleted from future budgets.

- I’ve adjusted my net income to reflect my current income, and the free cash flow calculation flows as expected from net income minus expenses.

If I’m successful in sticking to this budget, it will represent a 19.4% reduction in spending from this end of year review, as well as leave me enough free cash flow to max out my IRA in the first half of the year. I’ve also made myself a note to start contributing to a dependent care FSA when baby is born, so we can get some pre-tax dollars contributed and use the tax savings to offset some daycare spending.

Savings Check-up

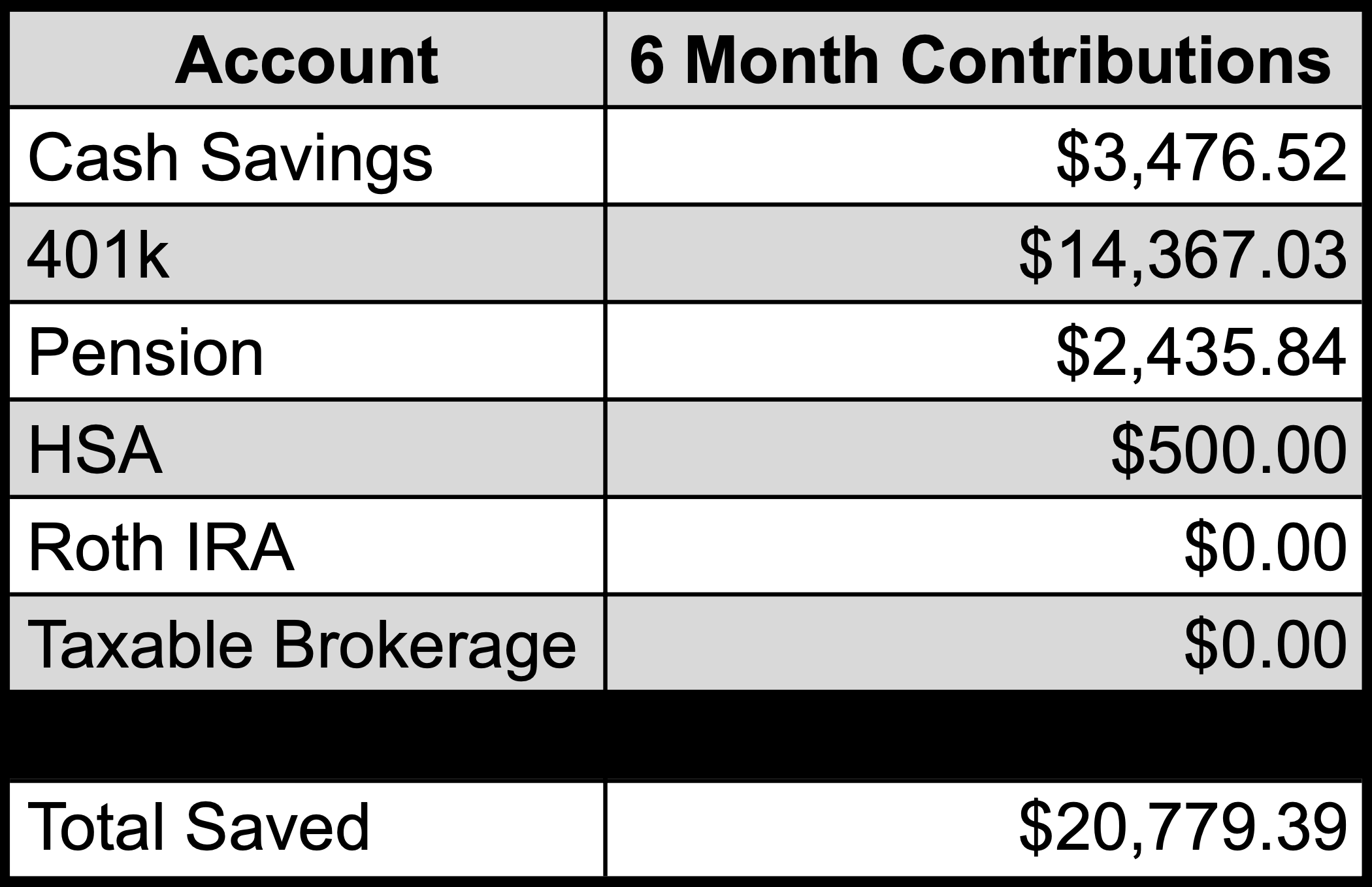

Let’s take a look at my total cash inflows to savings and investment accounts over the past 6 months:

Despite my high expenses I still managed some respectable savings, although it’s more on par with how much I was saving when I started this blog in 2019 than some of the recent years where I managed to save over $30k in some six month periods. Happy to have my 401k maxed out through automatic paycheck deductions so this budget bust did not turn into a savings bust!

To close out 2025, I had $48,800 in total annual savings when adding in what I saved during the first half of the year. A lot of my portfolio growth is still coming from contributions at this stage.

Net Worth Check-up

June 30, 2025 Net Worth: $644,274

December 31, 2025 Net Worth: $713,634

6 Month Change: $69,360

Wow, apparently I rocketed over a $700k net worth for the first time ever! My net worth has doubled in two and a half years — it was $355k at the 2023 mid-year check in. A lot of this was savings, but I just checked and the S&P 500 is up 56% over that same period.

I haven’t bothered looking at the stock market in so long that I had zero clue the S&P 500 index was close to hitting 7,000 points. I also must have slept through that ~20% pullback from 6,150 to 5,000 points in the spring of 2025, because I didn’t notice that either until just checking the chart. Sometimes it’s beneficial to disconnect, but I think the overall lesson of this budget review is that I need to find a good balance of autopilot with my savings and investments, and conscious management of my spending and budget.

Time to leave 2025’s finances in the past — aside from filing taxes in a few weeks — and I’m looking forward to everything 2026 will bring!

Congrats !